What is trade receivables securitisation?

Trade receivables securitisation is a way for large corporates to sell pools of their outstanding invoices on the capital markets, creating a new source of funding. A seller of products will pool their invoices within a special purpose vehicle (SPV) which in turn will issue securities or notes to investors, the proceeds of which are used to fund the ongoing purchase of receivables.

Investors will commit to purchase the notes for up to five years against a formula that considers dilution and loss history. It is ideal for companies with large numbers of customers and can aggregate receivables from operating companies across different geographies and business units.

How does Trade Receivables Securitisation work?

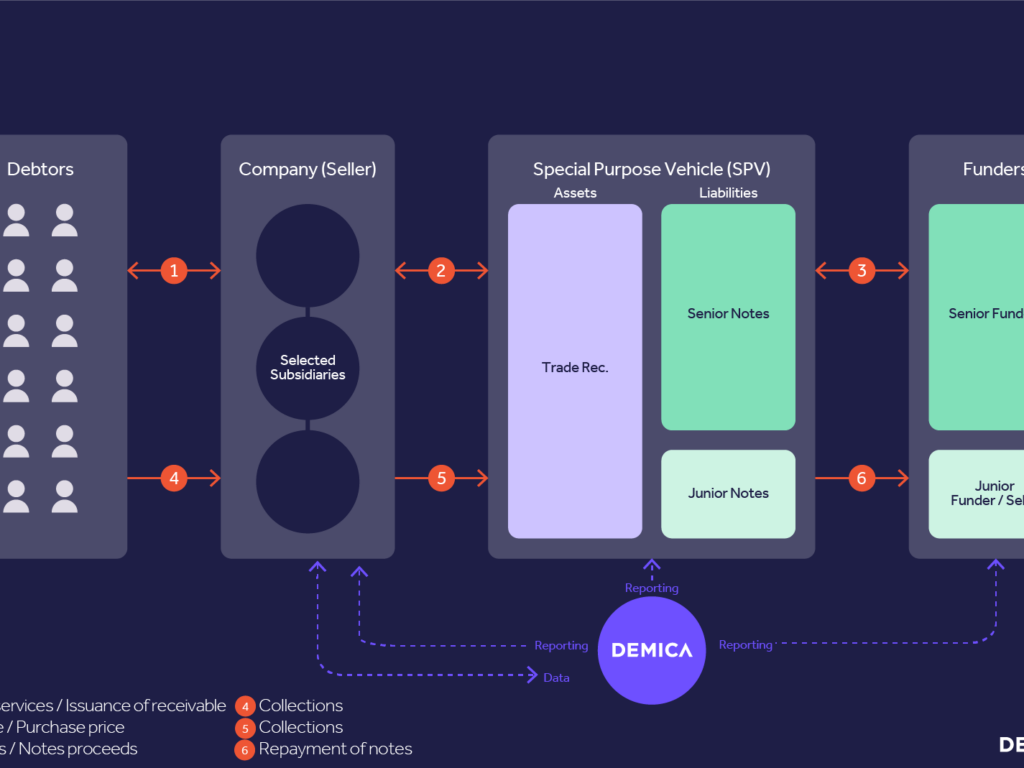

The difference between a trade receivables securitisation transaction and a more basic receivables financing is the introduction of a special purpose vehicle (SPV) into the process.

1. Sales of goods and services / Issuance of receivables

A company or group of companies (sellers) supply their goods and services to their clients (debtors) domestically or internationally. The sellers will issue invoices to the debtors, with payment terms ranging from 30-90 days – this creates a working capital need for the sellers.

The sellers will then contact funders, who will fund these trade receivables. The funders don’t purchase the receivables directly from the seller, but provide finance by purchasing notes or providing loans and for that reason an SPV is created. This is a legal entity whose sole purpose is to buy receivables from the sellers.

2. Issuance of notes / Notes proceeds

The SPV will issue notes that are securities secured by the trade receivables. These notes represent the economic value of the invoices and are subscribed to by investors who provide funding to the SPV.

3. Sale of receivables / Purchase price

The SPV pays the purchase price of the receivables to the sellers.

4. Collections

On the due date, the debtors will pay the value of the receivables to the seller, who keep the commercial relationship with their clients and continue servicing receivables.

5. Collections

These collections will then be sent to the SPV who will then purchase new receivables. Receivables are normally purchased on a weekly basis but can be purchased as often as daily.

6. Repayment of notes

If there are less receivables to purchase or the programme ends, then the collections are used to repay the notes to the investors.

What are the benefits of Trade Receivables Securitisation?

There are many benefits to a trade receivables securitisation programme which can result in greater profitability for your business and help meet your financial objectives. We have identified the main benefits below:

Stable, long-term source of financing A securitisation facility based on a global receivables portfolio owned by the SPV typically benefits from a two to five-year financing commitment from investors.

A single facility for all your operating companies The pooling of receivables (across operational entities, currencies and countries) enables the treasury team to have a global view on the receivables’ performance. Due to the assessment at portfolio level (and not at operating company level), the performance of the receivables is more stable resulting in an optimised financing level for all companies.

Competitive funding cost A trade receivables securitisation programme enables access to deeply liquid capital markets and its set up costs can typically be amortised over several years.

Highly scalable A trade receivables securitisation programme makes it easy to add new operating companies and investors over the life of the programme.

What should be considered when starting a Trade Receivables Securitisation programme?

There are a number of factors that a company should consider when embarking on a trade receivables securitisation programme, from whether your company generates revenues above $50m to having a wide enough customer base that generates a large volume of invoices. We’ve highlighted three key considerations below:

Would you like to diversify your source of funding?

Rather than going through the traditional route of obtaining finance through a direct route to a bank, a trade receivables securitisation transaction is financed through capital markets, which allows access to broader investors and allows the company to keep its financing facilities with its banks for other purposes..

Do you operate subsidiaries in multiple countries?

A trade receivables securitisation programme is a great way of obtaining finance for all your subsidiaries under one umbrella, as the SPV acts as a separate entity to your company – dealing with funders from one location. The SPV will then redistribute funds to the relevant subsidiary.

Do you need to start the programme immediately?

Due to the complexities involved in some transactions and the need to set up the SPV entity, a trade receivables securitisation programme can take up to three months to set up. However once set up, there is relatively little maintenance needed to run the programme.

Why run your trade receivables securitisation with Demica?

How we helped TreviPay

Learn how a Trade Receivables Securitisation programme powered by Demica unlocked $215m for fintech, TreviPay.

Related articles

Trade Receivables Securitisation

Expert guide to Trade Receivables Securitisation